")

Darren 415

I wrote about Ascend Wellness (OTCQX:AAWH) in early November and said it was no longer the cheapest MSO. At the time, the stock was trading at just $1.00, but now it trades at a much higher price. But I like it! To be honest, I liked it back then too. I was worried that the price was not so cheap compared to other companies in the same industry.

In this follow-up, we review the fourth quarter and 2023 financial results, discuss the outlook and how it has changed, and look at charts to evaluate the valuation. Hopefully, with the analysis I share, AAWH now makes up 19% of my “Beat the American Cannabis Operator Index” model portfolio and now the “Beat the Global Cannabis Stock Index” I hope this explains why it accounts for 6% of the model portfolio. I added some last week, including one I bought on Friday for $1.30.

Ascend Wellness Improved in 2023

Ascend Wellness’ 2023 net revenue increased 28% to $518.6 million. Gross profit margin fell from his 33.1% to 29.9%. Fortunately, operating expenses only increased by 12%, partly because there were no closing costs. Excluding his $5 million charge from 2022 results, operating expenses increased 16%. Adjusted EBITDA for the year expanded 14% to $106.5 million. One of the biggest improvements was in operating cash flow, which expanded from negative $38.4 million in 2022 to $75.3 million. Capital expenditures were $24.2 million, and the company generated free cash flow. The 2024 10-K includes projected capital expenditures of $35 million to $40 million.

I like that Ascend Wellness isn’t present in as many states as other MSOs. That’s because Ascend Wellness could expand or be acquired by a larger MSO. Many investors fail to understand that multiple states place restrictions on operators. Some are limiting the number of dispensaries, while others are capping the size of cultivation facilities.

Ascend is based in New York City and has operations in Illinois, Maryland (non-growing), Massachusetts, Michigan, New Jersey, Ohio, and Pennsylvania. Illinois has endured some challenges in 2023, with dispensaries capped at 10 stores and adult-use legalization in Missouri. Two of his stores were near the Missouri border and benefited from tourist purchases.

Aiding Ascend in 2023 was New Jersey’s adult-use legalization, which took effect in April 2022. The Maryland acquisition expands the range from medical to adult use. Ohio plans to legalize adult use, and Pennsylvania may do the same.

One thing I don’t like about Ascend and many of its peers is that they have negative tangible book value despite having a lot of debt. I think it will be difficult to refinance the debt. Ascend ended 2023 with net debt of $236 million. Tangible capital was -$126.1 million.

Ascend Wellness’ outlook brightens

Prior to the fourth-quarter report, analysts had expected revenue of $576 million in 2024, Sentieo said. Adjusted EBITDA was expected to be $121 million. Analysts now expect revenue to increase 11% to $576 million, while adjusted EBITDA is expected to increase 17% to $124 million. The average revenue growth rate for Tier 1 and Tier 2 companies is just 4.5%, and Ascend is projected to have the highest growth of these companies, so Ascend Wellness has better growth forecasts than its peers this year. It will be expensive. Ascend’s adjusted EBITDA growth rate is the second highest, well above the average of 10%.

Two out of nine analysts expected 2025 sales of $589 million and adjusted EBITDA of $139 million. Five analysts currently expect sales to rise 7% to $617 million.

Ascend Wellness has a fascinating chart

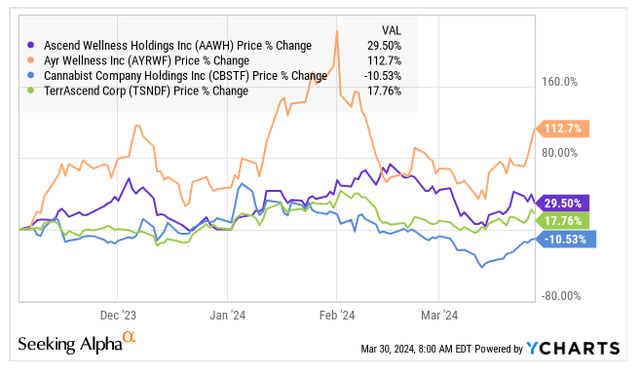

AAWH is up 29.5% year to date in 2024. This is slightly ahead of the New Cannabis Ventures Global Cannabis Stock Index, which is up 26.0% year-to-date. AAWH was not included in the index in the first quarter, but was added to the index in the second quarter due to increased trading volume.

Compared to MSO, Ascend lags behind. The NCV American Cannabis Operator Index, which includes NCV and 12 other MSOs, rose 34.9% through the first quarter of 2024.

Looking at Ascend’s performance compared to three other Tier 2 MSO names since early November, it has significantly underperformed AYR Wellness (OTCQX:AYRWF). Outperformed the other two.

Y chart

I like Cannabist (OTCQX:CBSTF). Recent sales of convertible bonds weighed on the stock price. I wrote positively about his TerrAscend (OTCQX:TSNDF), but I no longer include him in my modeling portfolio.

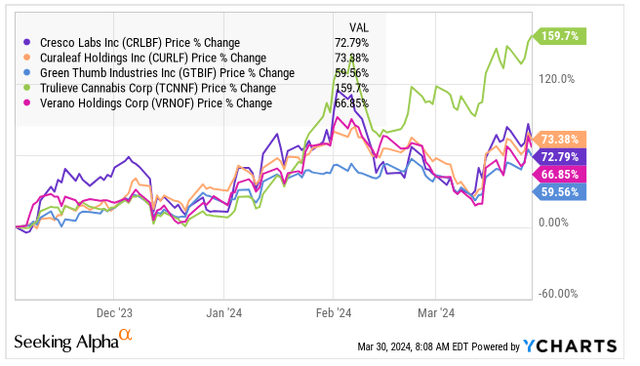

Looking at larger peers, all five names in Tier 1 have performed significantly better than AAWH since November 3rd. The worst name earned him more than twice as much as Ascend Wellness.

Y chart

AdvisorShares Pure US Cannabis ETF (MSOS) is up 70.2% since November 3rd. After that, the ETF no longer owned AAWH. It currently holds 1.9 million shares, which is only 0.2% of the total fund. The company first bought more than 1 million shares in early February, when the stock price was much higher than it is now.

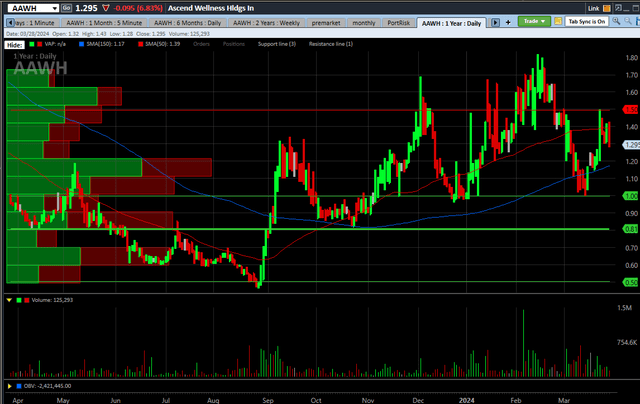

I think Ascend’s chart is attractive because it shows higher lows, higher highs, and has shown very high volume recently.

schwab

The large spike in trading volume in early February may be related to the acquisition by MSOS, but trading volume remains relatively high.

The stock hit an all-time low in late August, just before news of a potential schedule change was announced. It peaked in February and dropped back down to $1.00, but this looks like solid support at the moment. For now, I see $1.50 as potential short-term resistance.

If you look at the past two years, the stock price is still significantly lower.

schwab

The stock has only risen 12.6% since the end of 2022, well below the 45.3% rise in the U.S. Cannabis Operators Index.

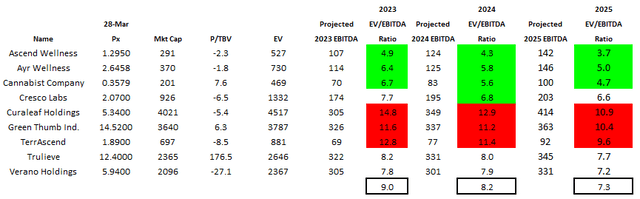

Ascend Wellness is once again inexpensive for MSO peers

In November, I pointed out that while Ascend was cheap, it wasn’t as noticeable as it used to be. Its enterprise value to 2024 expected adjusted EBITDA ratio was 3.7 times, the second lowest level among the nine Tier 1 and Tier 2 companies. The group average at the time was 5.5x.

Updated data for both 2024 and 2025 is below.

Alan Brochstein with Sentieo

Ascend is currently the cheapest at 4.3x in 2024 estimates. The current average is 8.2x, which is significantly higher than before. Estimates for AAWH rose, but were below price. However, peers have seen declining adjusted EBITDA estimates and significantly higher prices.

For 2025, Ascend is also the cheapest at just 3.7x. The average is 7.3 times. If cannabis becomes Schedule 3, the 280E tax will be abolished. This is very good for MSOs, potentially allowing them to expand their valuations.

Prior to our fourth quarter report, I shared a set of goals through the end of 2024 with members of our investment group. My optimistic target was $3.89 and my pessimistic target was $0.78 assuming 280E was gone. Updating these targets using the same metrics yields an optimistic target based on an enterprise value of $4.00, 8x projected 2025 Adjusted EBITDA. This is an increase of 209%. My pessimistic target, assuming a 3x decline, would be $0.84, representing a 35% downside potential. This is much better than other products.

conclusion

Ascend has risen significantly since early November, but the gains have been smaller than its MSO peers. To them, the stock looks relatively cheap. How the rescheduling plays out will have a big impact on its returns, but I like it enough to include it in my model portfolio.

We discussed the company’s attractive chart and cheap valuation compared to its peers. It is currently included in the Global Cannabis Stock Index that I am trying to beat in my model portfolio, but I am slightly overweight relative to that index.

The biggest risk to AAWH and its peers is if 280E does not disappear. As mentioned above, AAWH has a negative tangible book value and a large amount of debt, which will put pressure on the stock price. Another risk is that Pennsylvania, where many people are expected to move beyond medical marijuana to adult use, won’t do so.

Two weeks after I wrote this article on Ascend, I reiterated my bullish stance on Trulieve (OTCQX:TCNNF), which at the time was priced at $5.61, compared to the price at which I valued Ascend at $4.775. rose from the dollar. It has more than doubled! We recently downgraded TCNNF to “sell”. I think AAWH is a good alternative to TCNNF, which has fewer positives and more negatives than Ascend Wellness.

So while I’m not a fan of MSOs at the moment due to concerns that investors are getting overly excited about something that may not happen, I rate this MSO a Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.