unstable earnings are just the beginning of the problem")

The latest earnings report is Starjoy Wellness and Travel Company Limited (HKG:3662 ) Investors were disappointed. After doing some research, we believe that the situation is better than it appears due to several encouraging factors.

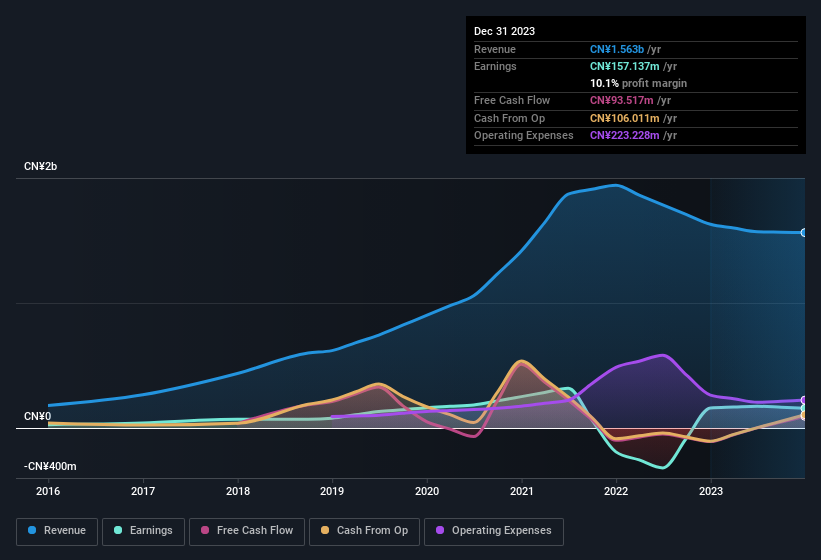

Check out our latest analysis for Starjoy Wellness and Travel.

An examination of Starjoy Wellness and Travel’s cash flow relative to its earnings.

In high finance, a key ratio used to measure how well a company converts its reported profits into free cash flow (FCF) is: Incidence (from cash flow). The accrual ratio subtracts his FCF from the profit for a particular period and divides the result by the company’s average operating assets for that period. You can think of the accrual rate from cash flow as the “non-FCF rate of return.”

So if a company has a negative accrual ratio, it’s actually a good thing, and if the accrual ratio is positive, it’s a bad thing. This does not suggest that you need to worry about positive accrual rates, but it is worth noting if the accrual rate is fairly high. In particular, there is some academic evidence to suggest that, generally speaking, high accrual rates bode poorly for short-term profits.

For the twelve months ending December 2023, Starjoy Wellness and Travel had an accrual ratio of 0.23. Unfortunately, this means that free cash flow was significantly lower than reported profits. In fact, his free cash flow over the last twelve months was CA$94.0m, significantly lower than her CA$157.1m in profit. Notably, Starjoy Wellness & Travel had negative free cash flow last year, so generating CA$94m this year is a welcome improvement. That being said, there’s more to the story. We can see that the unusual items are impacting the statutory profit and therefore impacting the accrual ratio.

Note: Investors are always advised to check the health of a company’s balance sheet. Click here to see Starjoy Wellness and Travel’s balance sheet analysis.

How do unusual items affect profits?

Unfortunately (in the short term), Starjoy Wellness and Travel suffered a loss in profits due to C$24 million worth of exotic products. If this were a non-cash claim, it would have been easier to convert to higher cash, so it’s surprising that the accrual rate tells a different story. Losing points for unusual items is disappointing at first, but there is a silver lining. Our analysis of the vast majority of publicly traded companies around the world shows that significant abnormal items often do not repeat. This is not surprising since these line items are considered rare. So, assuming these unusual expenses don’t occur again, we expect Starjoy Wellness and Travel to generate higher profits next year, all else being equal.

Our view of Starjoy Wellness and Travel’s profit performance

In conclusion, Starjoy Wellness and Travel’s accrual ratio suggests that its statutory profit is not backed by cash flow, even if unusual items weigh on profits. Given these contrasting considerations, we do not have a strong view as to whether Starjoy Wellness and Travel’s earnings adequately reflect its underlying profit potential. If you want to know more about Starjoy Wellness and Travel as a business, it’s important to be aware of the risks the company faces. After doing some research, we found the following: 3 warning signs for Starjoy Wellness and Travel (Two of which make us uncomfortable!) We think they deserve our full attention.

Our research on Starjoy Wellness and Travel focused on certain factors that could make its earnings look better than they actually are. But there are many other ways to communicate your opinion about a company. For example, many people consider a high return on equity to be a sign of good economic conditions, while others like to ‘follow the money’ and look for stocks that insiders are buying.It may take a little research on your behalf, but you may find the following free A collection of companies with a high return on equity, or a list of stocks that insiders are buying to help.

Valuation is complex, but we help make it simple.

Please check it out Starjoy Wellness and Travel Could be overvalued or undervalued, check out our comprehensive analysis. Fair value estimates, risks and caveats, dividends, insider trading, and financial health.

See free analysis

Have feedback on this article? Interested in its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.