")

Daniel Griselli

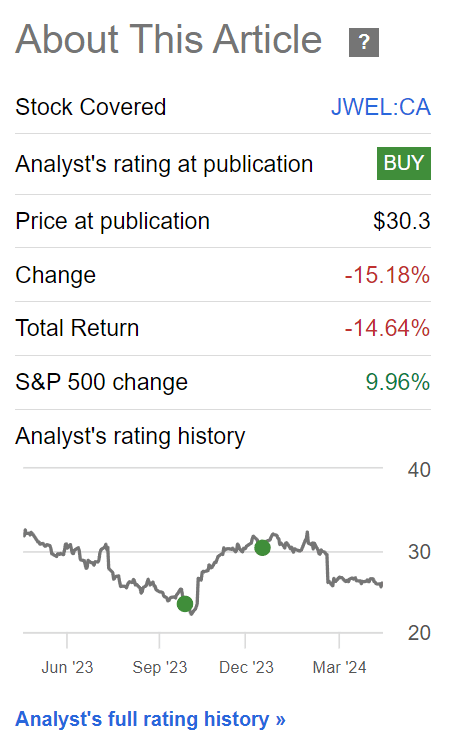

My previous article on Jamison Wellness (TSX:JWEL:CA) (OTCPK:JWLLF), I rate the company a Buy based on its strong international growth outlook and the company’s valuation discount compared to its Consumer Staple peers.

But it’s not in stock yet It has performed as expected, falling 15% since January (Figure 1).

Figure 1 – JWEL has fallen 15% since the last update (In search of alpha)

What happened to Jamison Wellness? Do the company’s growth prospects still hold?

Jamieson’s stock price fell in March after the company reported fourth-quarter 2023 results and gave a weaker-than-expected initial outlook for 2024. In particular, the company had a weak year in its contract manufacturing business, which came as a surprise to investors.

Turning to its recent first-quarter earnings report, Jamieson’s results were mixed as a month-long labor dispute disrupted manufacturing. distribution. The company had to divert resources to maintain delivery of branded products, leading to a decline in overall revenue.

At this point, I’m encouraged by strong growth in the US and China, so I’d give the company the benefit of the doubt. Assuming sales delays in Canada and overseas can be recovered in the coming quarters, Jamieson should be able to beat his conservative guidance.

(Author’s note, financial figures in this article are in Canadian dollars)

Company Profile

Jamison Wellness is a company that doesn’t get much press, so I’d like to take a few paragraphs to briefly review the company’s business for those new to the story. Jamieson is a leading Canadian manufacturer of vitamins, minerals and supplements (“VMS”). The company’s products are manufactured in-house and sold to consumers through more than 10,000 retail stores and major e-commerce platforms.

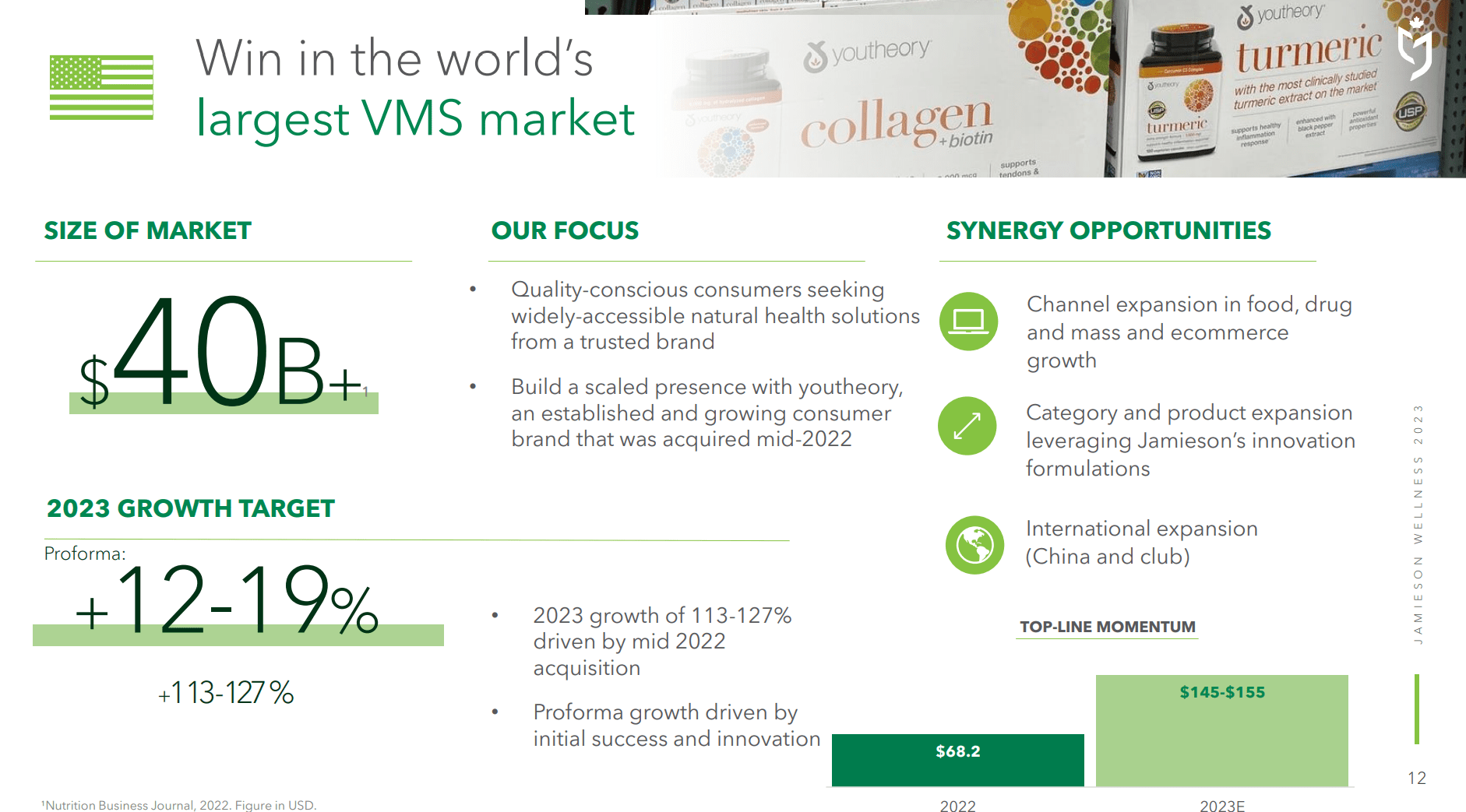

In recent years, as Canada’s VMS market has matured, Jamieson has looked overseas for growth. In order to tap into the large $40 billion US market, Jamison acquired health and beauty supplement brand You Theory in 2022 (Figure 2).

Figure 2 – The United States represents a large market for increasing market share (JWEL investor presentation)

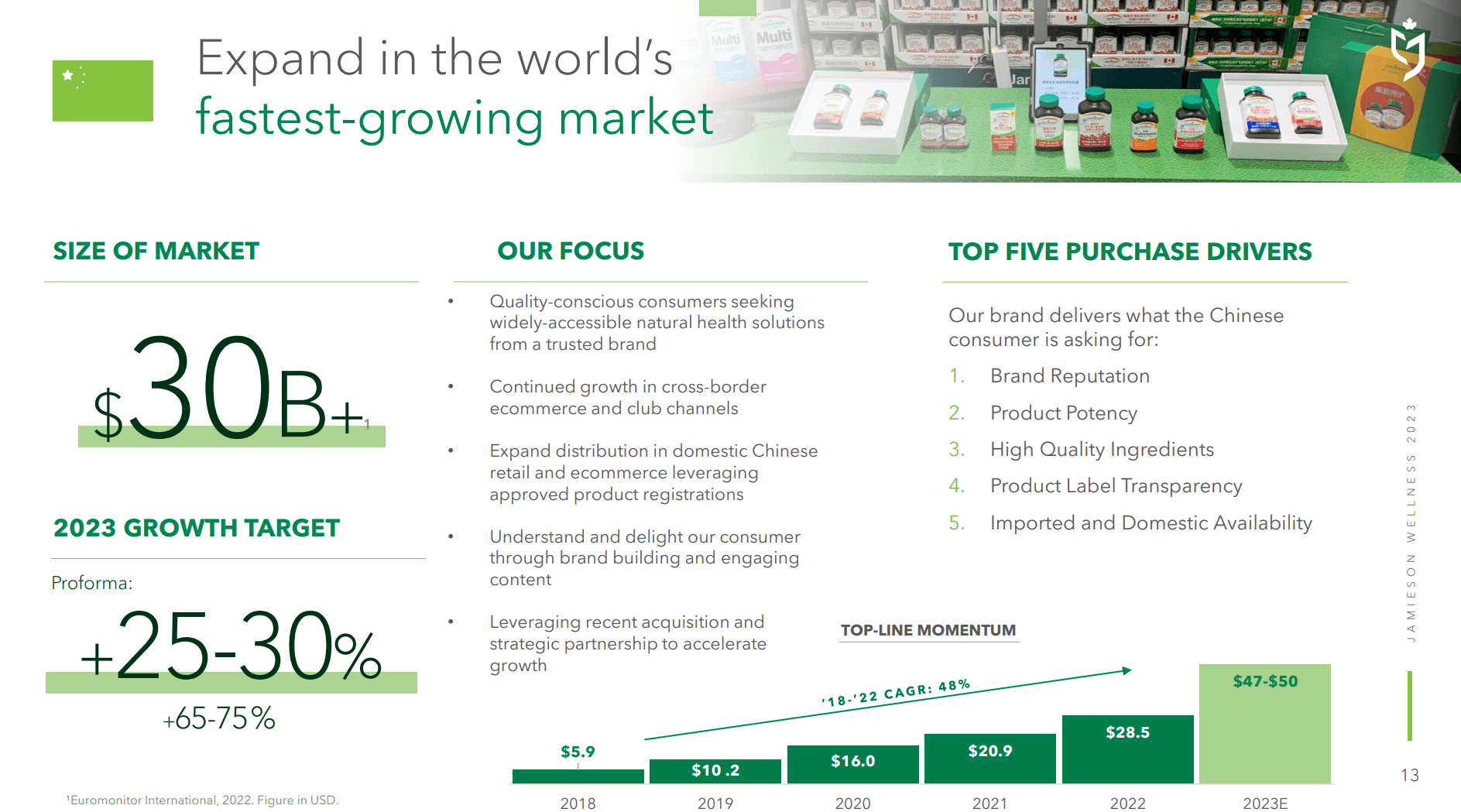

Jamieson is expanding its list of global distribution partners to other regions of the world. In China, an estimated $30 billion market, Jamieson recently acquired the assets of a distribution partner and is looking to expand locally (Figure 3).

Figure 3 – JWEL continues strong growth in China (JWEL investor presentation)

Lackluster guidance led to stock price decline

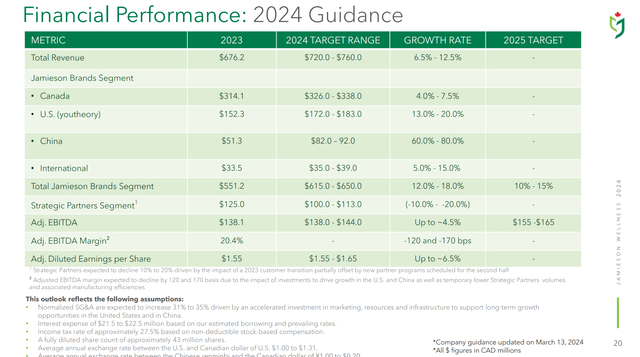

Investors in growth stocks like Mr. Jamison often expect and demand strong double-digit growth in revenue and profits. However, in its 2023 Q4 earnings release in March, Jamison also announced lower-than-expected preliminary guidance for 2024, with 2024 revenue forecast of $720 million to $760 million (up 6.5% to 12.5%). ), adjusted for $720 million (up 6.5-12.5%). Dill. EPS of $1.55 to $1.65 (up approximately 6.5%) (Figure 4).

Figure 4 – JWEL 2024 Guidance (JWEL investor presentation)

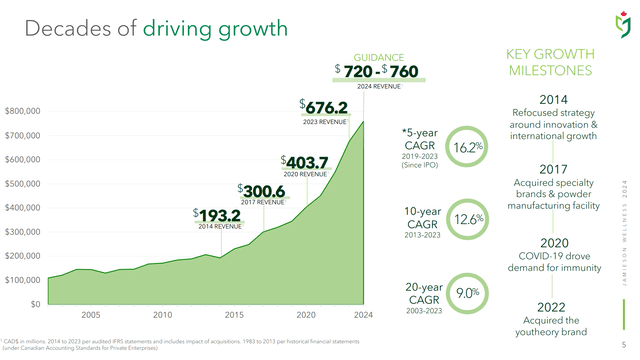

The 6-12% growth is in line with the company’s 20-year revenue CAGR, but is noticeably slower than the 16% CAGR growth over the past five years (Figure 5).

Figure 5 – JWEL Compounded 16% Over the Past 5 Years (JWEL investor presentation)

Particularly because Jamieson expected its 2024 sales to be only $100-113 million, or a 10-20% decline in comparison Investors were surprised by the expected decline in the company’s contract manufacturing business. Achieve 15% growth by 2023. Jamieson explained that Strategic Partners’ revenue decline was due to the migration of large customers.

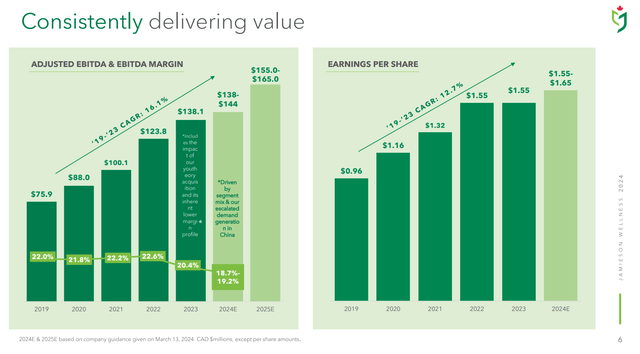

The adjusted EBITDA guidance of $138 million to $144 million (+~4.5%) was also inconsistent with the company’s historical growth formula of adjusted double digits. EBITDA and adjusted EPS CAGR (Figure 6).

Figure 6 – Adjusted EBITDA guidance was not consistent with historical growth (JWEL investor presentation)

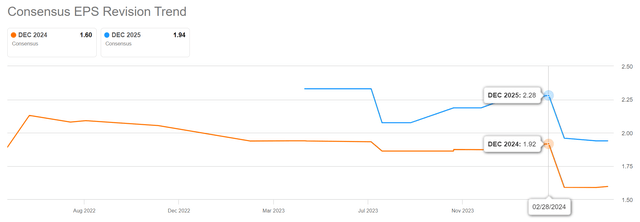

In fact, before the guidance was released, analysts were expecting EPS of $1.92 per share in 2024 (Figure 7).

Figure 7 – Consensus EPS Revision Trend (In search of alpha)

First quarter marred by labor movement

Mr. Jamieson’s weak leadership was compounded by a worker strike that affected the company’s manufacturing and warehousing operations in Windsor, Ont., for more than a month.

Although the labor strike was ultimately resolved with Jamison offering a 20.5% wage increase over four years and a large contract bonus, the labor lawsuit caused significant disruption to Jamison’s operations, and the company’s strong first quarter It ruined our financial performance.

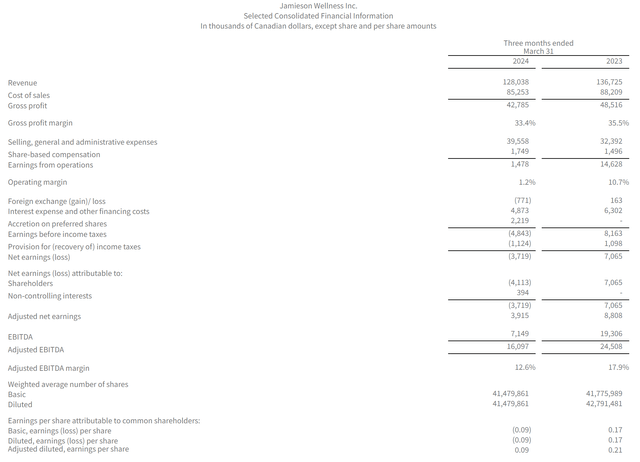

For the quarter, Jamison reported revenue of $128 million, up 6.4% year over year. decline,Profit margins were also negatively impacted, with gross margin of 33.4% (35.5% year-over-year) compared to an adjusted 33.4% (35.5% year-over-year). EBITDA margin was 12.6% (17.9% YoY) (Figure 8).

Figure 8 – JWEL Q24 Q1 Financial Summary (JWEL Q1/24 press release)

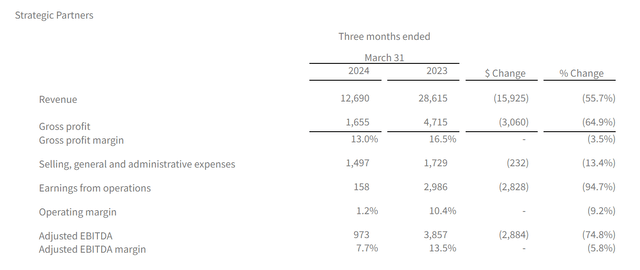

Importantly, Jamison had to divert resources from its strategic partnership business to fulfill orders for its branded business, resulting in a significant 56% year-over-year decline in strategic partners’ revenue, resulting in a operating profit margin decreased to 1.2% (Figure 9).

Figure 9 – Strategic Partnerships Segment, Q1 2024 (JWEL Q1/24 press release)

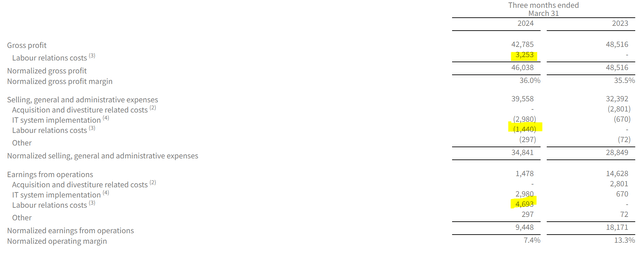

In addition, the labor strike resulted in a one-time charge of $9.4 million across cost of goods sold and selling, general and administrative expenses, which negatively impacted our first quarter results (Figure 10).

Figure 10 – Workers’ strikes result in large one-time costs (JWEL Q1/24 press release)

Core brand business maintains momentum

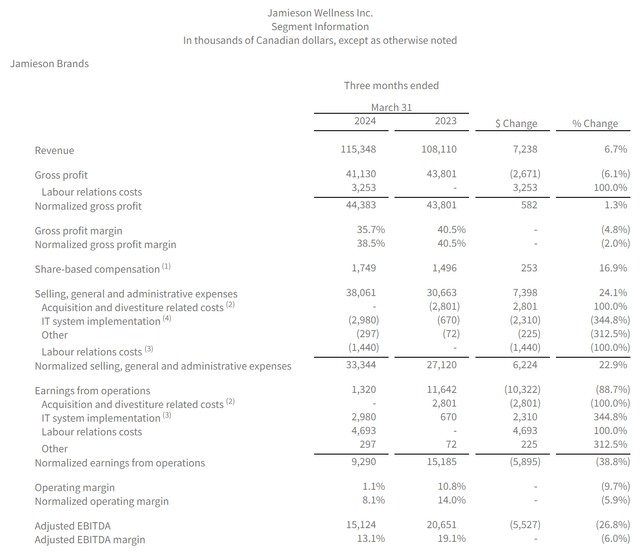

Despite the disruption caused by the 34-day strike, Jamison was able to divert resources from its contract manufacturing business and maintain deliveries for its private label business. This resulted in a 6.7% year-over-year increase in brand revenue. However, as mentioned earlier, segment revenues were negatively impacted by the disruption (Figure 10).

Figure 10 – Brand segments in Q1 2024 (JWEL Q12/24 press release)

Canadian and international revenue decreased 14.7% year over year to $60.9 million and 17.2% year over year to $5.3 million, respectively, as some first-quarter shipments were delayed to the second quarter due to the strike.

But on the bright side, U.S. revenue rose 37% year-over-year to $30.4 million, driven by innovative products and investments in demand generation. China was another bright spot, with sales increasing 126% year-on-year to $18.7 million, reflecting a shift to an owned distribution model. Excluding currency effects, China’s growth rate was 80% year-on-year.

Because the strike was resolved in a relatively short period of time, Jamieson believes he can get product shipments back and maintain his full-year outlook for the time being.

Consider recent volatility

For now, we recommend investors ignore recent changes in the company’s stock price and financial performance, particularly the decline in revenue from strategic partnerships. While any decline is not desirable, investors should focus on the fact that the gross margin (and profit contribution) of branded products is much higher compared to contract manufacturing. In fact, I couldn’t be happier if Jamieson could fill its entire manufacturing capacity with branded production and discontinue contract manufacturing altogether.

We are particularly encouraged by You Theory’s strong growth, as first quarter sales growth was 37% year-over-year, well above the company’s guidance of 13-20%. China is also growing at the upper end of its guidance. If first-quarter shipments to Canada and overseas can be made up in coming quarters, there’s a good chance Jamieson could beat the conservative guidance he set in March.

Valuation discount remains

Based on management guidance and analyst consensus adjusted estimates. Dill. With EPS of $1.60, Jamieson currently trades at his Fwd P/E of 16.1x compared to his consumer staples peers of 19.1x (Figure 11).

Figure 11 – JWEL evaluation (In search of alpha)

I believe Jamieson’s fair value is about 19x Fwd P/E, or about $30 per share.

Is growth on track?

In my opinion, the main risk for Jamieson at the moment is growth. Jamison is highly sensitive to growth surprises, as evidenced by the stock’s reaction to the 2023 Q4 earnings report and his initial 2024 outlook. This may be due to the fact that Jamison has historically been a “growth at a fair price” (“GARP”) story and is held by GARP-focused investors. If the company can continue its branded product momentum throughout the year, I believe shareholders will be well rewarded.

Conversely, if growth slows, shareholders may be caught off guard, as growth stocks without growth are often severely punished.

conclusion

For now, I’m going to take a profit on Jamieson Wellness and ignore its recent messy first-quarter earnings report, as financial results were hurt by a labor strike that disrupted manufacturing and shipping for the quarter. is.

The brand’s growth appears to be stronger than initially expected, especially in the United States, which has been a pain for the company since its pricey acquisition of Useory. China is also growing very rapidly.

i am maintaining buy Recommended at this time.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.