Target price is USD 3.00")

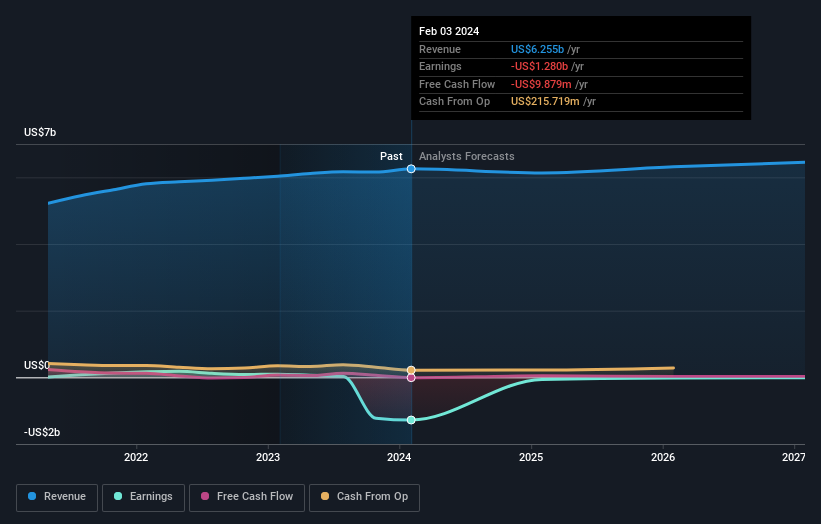

It was a normal week Petco Health and Wellness Company, Inc. (NASDAQ:WOOF), whose stock price fell 14% to $1.95 in the week since its latest annual results. The statutory results were not great. Revenues of US$6.3 billion matched expectations, but Petco Health and Wellness Company lost US$4.78 per share in the process. This is an important time for investors, as they can track a company’s performance in the report, see what experts predict for next year, and see if there have been any changes to expectations for the business. With this in mind, we’ve gathered the latest statutory forecasts to find out what analysts are expecting for next year.

Check out our latest analysis for Petco Health and Wellness Company.

Following last week’s earnings report, Petco Health & Wellness Company’s 15 analysts now expect 2025 revenue to be US$6.13b, about the same as the previous 12 months. Losses are expected to decrease significantly, shrinking by 96% to US$0.21. Prior to this latest report, consensus had been expecting revenue of US$6.13b and loss of US$0.24 per share. While earnings estimates remain largely unchanged, sentiment appears to have improved, with analysts revising numbers upwards, with losses per share in particular improving markedly.

Despite the lower expected loss, analysts lowered the company’s valuation, with the average price target dropping 7.7% to $3.00. Analysts appear to be less optimistic about the business overall. However, it is unwise to stick to a single price target, as the consensus target is effectively an average of analyst price targets. As a result, some investors like to look at a range of estimates to see if there is any disagreement regarding a company’s valuation. The most optimistic Petco Health and Wellness Company analyst has a price target of $6.00 per share, while the most pessimistic has a price target of $1.00 per share. So we don’t give much confidence to the analyst price targets in this case, as there are clearly widely differing views on what kind of performance this business could generate. As a result, basing decisions on consensus price targets may not be a good idea. After all, the price target is just an average of this wide range of estimates.

While these estimates are interesting, it can be helpful to paint a broader stroke when comparing Petco Health and Wellness Company’s past performance and forecasts with other companies in its industry. We would like to highlight that earnings are expected to reverse and decline by 2.0% per annum by the end of 2025. This is a notable change from the historic growth of 8.6% over the past five years. In contrast, our data shows that other companies in the same industry (covered by analysts) are forecast to see their revenue grow at 5.0% per year, for now. It’s clear that Petco Health and Wellness Company’s earnings are expected to be significantly worse than the industry as a whole.

conclusion

Most importantly, the analysts reaffirmed their loss per share forecasts for next year. Happily, the analysts also reaffirmed their earnings forecasts, suggesting things are in line with expectations. However, our data suggests that Petco Health and Wellness Company’s earnings are expected to be worse than the broader industry. Analysts don’t seem reassured by the latest results, with the consensus price target dropping significantly, leading to a reduction in Petco Health & Wellness Company’s future valuation.

Based on this idea, we think the long-term outlook for the business is far more relevant than next year’s earnings. His forecasts from multiple Petco Health and Wellness Company analysts out to 2027 are available for free on our platform here.

Still, keep in mind that Petco Health and Wellness Company says: 1 warning sign in investment analysis you should know…

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.